Episode 1

Why Most People Stay Broke

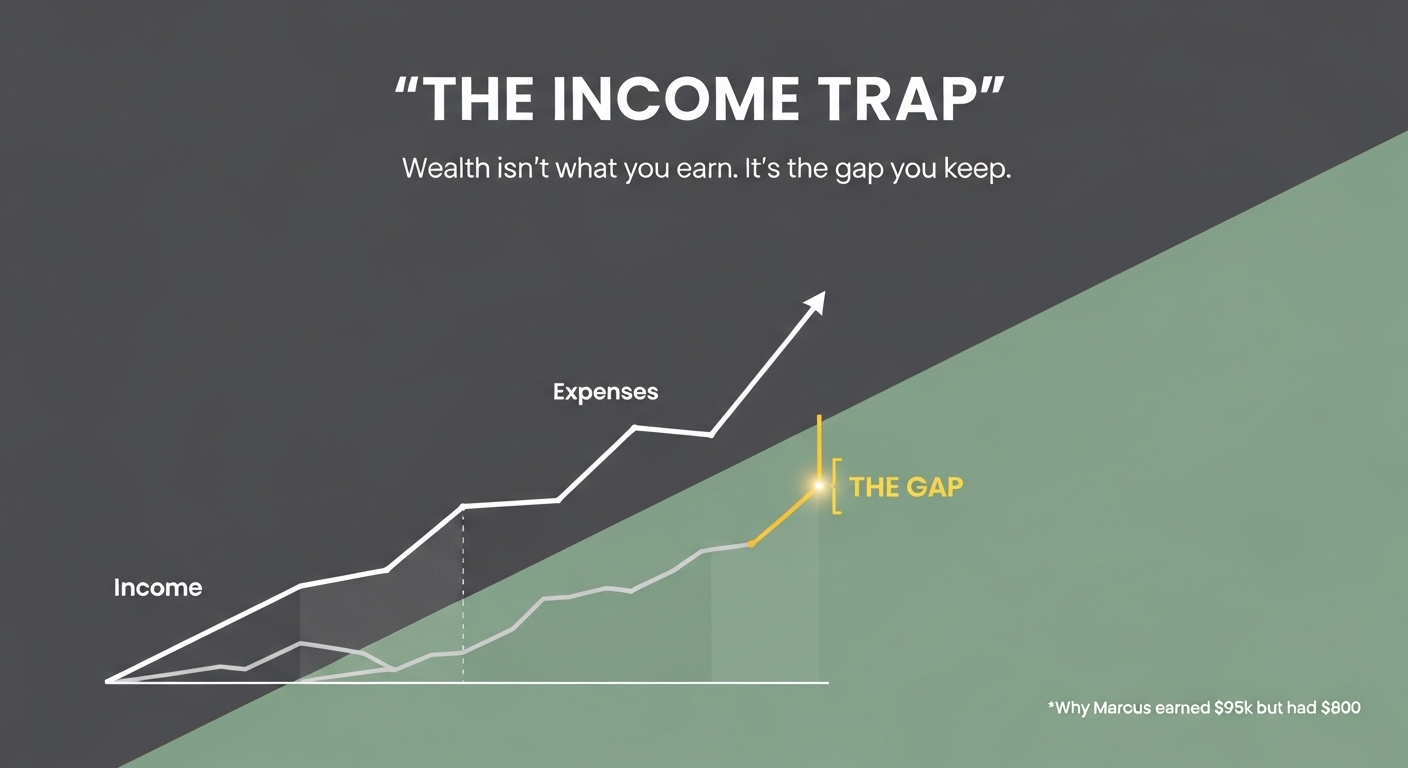

The Man Who Earned More and Had Less

Imagine Marcus

Imagine you are Marcus.

You grew up without much. You worked hard, got educated, landed a real job.

At 28, you're making $65,000 — more than anyone in your family ever saw. You feel like you made it.

By 34, you're earning $95,000. You've been promoted twice. You've outworked people who had more advantages than you.

You have $800 in savings.

Not because you were reckless.

Not because you didn't care.

Because every time money came in, life quietly expanded to absorb it.

- Better neighborhood

- Better car

- Better restaurants because now you had better friends

Each decision made sense in isolation.

The pattern was invisible until it wasn't.

The Truth Most People Miss

Here's what nobody told Marcus — and what most people never figure out:

Income rising does not automatically mean wealth building.

The gap between what you earn and what you spend is the only number that matters.

Do This First — Before You Read Another Word

Pull up your last 30 days of spending. Bank app, cash app, whatever you use.

Don't analyze it yet. Just look at it for 60 seconds.

Notice your first emotional reaction.

- Is it discomfort?

- Defensiveness?

- Numbness?

That reaction is the lesson.

That's your money psychology showing itself.

Hold that feeling — we're going to name it.

The Four Forces Keeping Most People Broke

1. Lifestyle Inflation

This is the Marcus trap.

Your income grows, your spending grows to match it — automatically, almost biologically.

You don't decide to inflate your lifestyle. It just happens when there's no competing decision already made.

The upgrade feels like a reward.

It feels earned.

That's what makes it dangerous.

2. The Spending vs. Income Gap

Wealth is not about how much you earn.

It's about the distance between what comes in and what goes out.

Someone earning $40,000 and spending $32,000 is building more wealth than someone earning $90,000 and spending $89,000.

The gap is everything.

Widening it — even by $200 a month — changes your trajectory.

3. Financial Avoidance

Most people don't track their money because tracking makes it real.

Avoidance feels like relief.

It is actually debt accumulating in the dark.

The discomfort you felt looking at those 30 days of transactions?

That's the exact feeling people spend years running from.

The ones who stop running are the ones who eventually get out.

4. Money Psychology

You don't make financial decisions with a spreadsheet.

You make them with your nervous system.

If money was scarce in your childhood, your brain learned that money is temporary — spend it before it disappears.

If you survived on almost nothing, "having enough" can feel unfamiliar, even suspicious.

These patterns run underneath every purchase.

You can't override what you haven't named.